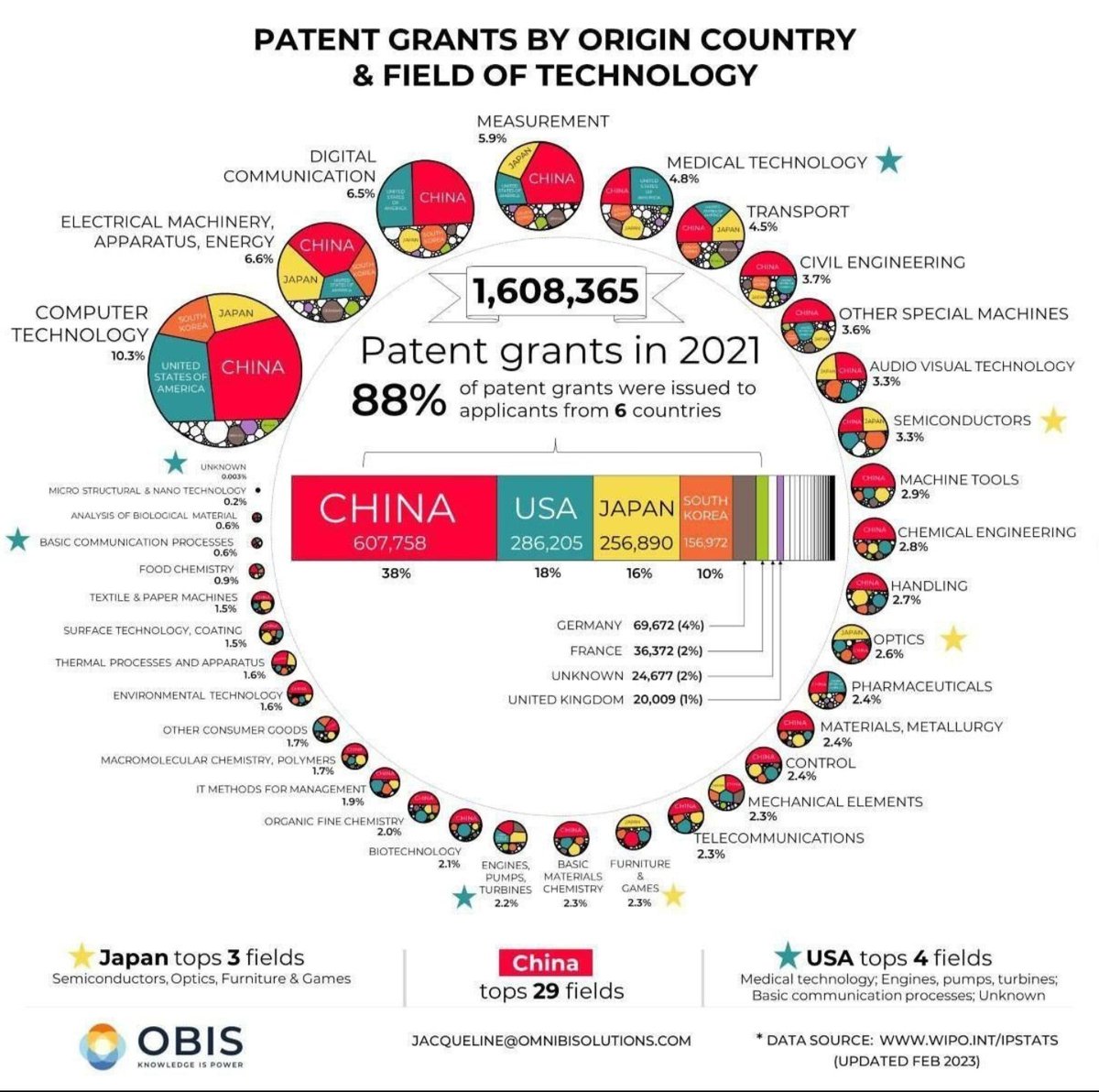

Wonder if "Unknown" is the sanctions friendly descriptor for Russia?

Military Forum for Russian and Global Defence Issues

Walther von Oldenburg likes this post

GarryB and kvs like this post

sepheronx and GarryB like this post

kvs likes this post

China’s solar exports have already drawn urgent responses. In the United States, the Biden administration has introduced subsidies that cover much of the cost of making solar panels and part of the much higher cost of installing them.

The alarm in Europe is particularly great. Officials are bitter that a dozen years ago, China subsidized its factories to make solar panels while European governments offered subsidies to buy panels made anywhere. That led to an explosion of consumer purchases from China that hurt Europe’s solar industry.

A wave of bankruptcies swept the European industry, leaving the continent largely dependent on Chinese products.

The remnants of Europe’s solar industry are now fading away. Norwegian Crystals, an important European producer of raw materials for solar panels, filed for bankruptcy last summer. Meyer Burger, a Swiss company, announced on Feb. 23 that it would halt production in the first half of March at its factory in Freiberg, Germany, and would try to raise money to complete factories in Colorado and Arizona.

GarryB and lancelot like this post

GarryB, kvs and lancelot like this post

kvs and ALAMO like this post

GarryB wrote:Video is unavailable.

Video is private.

GarryB, kvs and lancelot like this post

GarryB and lyle6 like this post

kvs likes this post

GarryB and lancelot like this post

|

|

|

ALAMO

ALAMO